INDUSTRIALIZATION

iii. The Post-Revolutionary Period, 1979-2000s

Industrial development in the post-Revolutionary period can be divided into two distinct phases. The first phase spans the 1980s covering the period from the 1979 Revolution to the end of the 1980s (including the war with Iraq during 1980-88). This period was influenced by external and internal shocks and beset by policy-induced distortions relating to the Revolution and war. In general, this phase was characterized by an ideologically oriented set of economic policies and, associated with them, the uncertainty surrounding the legitimacy of private property and the extent of permissible wealth accumulation in the Iranian economy.

In the second phase, which covers the period after the death of Ayatollah Khomeini in 1989, industrial policies aimed at rectifying imbalances that were created in the first phase. The three five-year development plans, which were formulated after the end of the Iran-Iraq war, have been concerned, inter alia, with the regeneration of the industrial sector. The success of these plans, however, has to be judged by the extent to which they have been able to address the endemic problems of the manufacturing industries in terms of low productivity, fragmentation, and international competitiveness.

STAGNATION

Manufacturing growth in the 1980s. There is a general consensus among observers of the Iranian economy that during the 1980s the manufacturing sector was largely neglected (Behdad, 2000; Hakimian and Karshenas, 2000; Pesaran, 2000; Amuzegar, 1997; Mazarei, 1996; Alizadeh, 1992; World Bank, 1991; Amirahmadi, 1990). Comprehensive data on the structure and performance of manufacturing enterprises during the 1980s are lacking. A World Bank report in 1991 points out that a combination of poor industrial performance, concentration on war economy, and overall neglect “also eroded the information base to assemble a coherent picture of the industrial sector” (1991, p. 52).

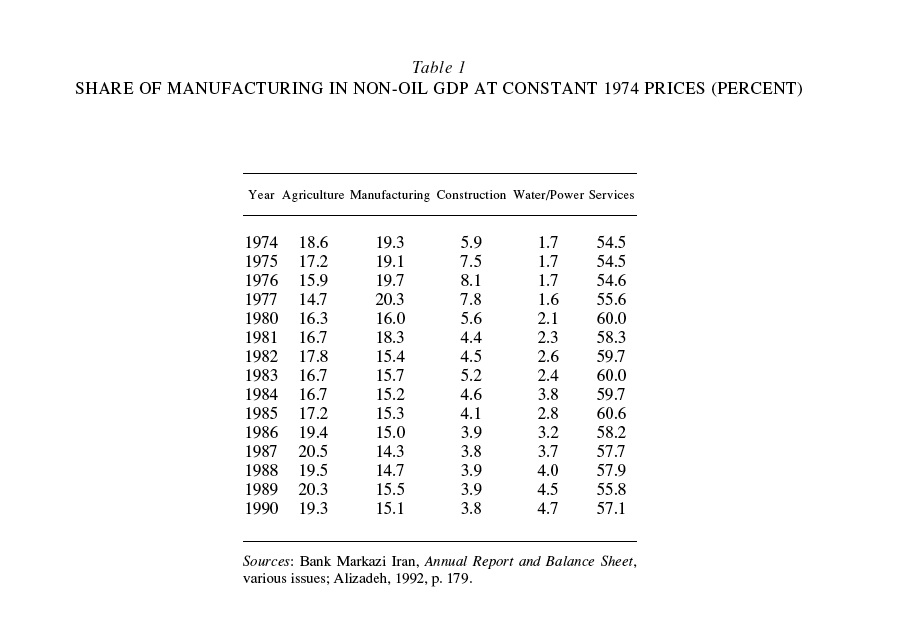

Available evidence, in fact, indicates that the share of the manufacturing sector in the economy declined after the Revolution (Table 1). The share of manufacturing, which was around 19-20 percent of non-oil GDP by 1977, dropped to about 15 percent by 1990. The share of agriculture in Iran’s non-oil GDP, however, increased over the same period.

{kind=link}

The decline of the manufacturing sector over this period reflected to a large extent the shift in political priorities in favor of agriculture after the Revolution (Amirahmadi, 1990; World Bank, 1991). This was partly a response to the industrial ‘bias’ associated with the previous regime’s concentration on industrial growth and partly an attempt to increase self-sufficiency in food in response to war and external trade sanctions (see ECONOMY x.; see also Conspiracy theories). External shocks too affected the industrial sector in this period. These included trade embargos and financial sanctions from abroad, redirection of resources into war economy during the Iran-Iraq War, and the dwindling oil prices in the mid-1980s (World Bank, 1991, pp. 52-65). Under the condition of foreign exchange constraint, which implied decline in the imports of raw materials and intermediate inputs, most manufacturing plants were working well below capacity.

Above all, perhaps, the manufacturing sector endured policy-induced distortions which emanated from the Revolution and war, but also reflected the pervasive ideological orientation of economic policymaking in this phase and the extent and nature of the state control in resource allocation at that time (Hakimian and Karshenas, 2000; Mazarei, 1996; Alizadeh, 1992).

Industrial policies in the 1980s. The bill for the Protection and Development of Iranian Industries (Qānun-e ḥemāyat o tawseʿa-ye ṣanāyeʿ-e Irān), which was passed by the Revolutionary Council (Šurā-ye enqelāb) in 1979, reflected the politicization of industrial policies in the wake of the Revolution. The bill was primarily concerned with redistribution of wealth, industrial self-sufficiency, and employment generation. The objectives of the bill included determination of workers’ wages according to Islamic doctrines, the expropriation of factories and properties of industrialists associated with the previous regime, state control of a large segment of basic industries, expansion of employment opportunities, reduction in dependence on foreign sources of supply, and protection of the private sector against foreign competition.

Nevertheless, Iranian industrial policies in the 1980s led to a virtually complete government control of the manufacturing sector (Behdad, 2000; Pesaran, 2000; Amuzegar, 1997; Mazarei, 1996; Alizadeh, 1992; World Bank, 1991).

The first major step which directly involved the government in ownership and management of the industrial sector was large-scale nationalization of virtually all medium- and large-scale modern manufacturing enterprises and the banking sector. The bill for nationalization was enacted in 1979. All the takeover sanctioned by the bill was by the state. There were significant takeovers by foundations, but they were of the firms not covered by the original bill.

Nationalization was first and foremost aimed at safeguarding the redistributive nature of the Revolution by undermining the economic power structure of the modern private sector (Mazarei, 1996). The modern private sector that was born out of the policy of import substitution in the 1960s and 1970s was associated with the old regime. Furthermore, the takeover of private enterprises by the state and foundations was also a response to the disruption in production after the Revolution. This was triggered by a number of factors, including the large exodus of owners or managers of private industrial enterprises, massive debt of these companies to the banking sector, acute labor unrest, uncertainty regarding the ownership and administration of abandoned companies, and political interference in the decision-making processes of these enterprises (Amuzegar, 1997). This environment left the state with little option but to nationalize these firms.

During the 1980s the role of the state in the economy was accentuated in response to the exigencies of a war economy under the condition of foreign exchange constraint which was induced by trade embargos and financial sanctions from abroad as well as the dwindling oil prices in the mid-1980s (Hakimian and Karshenas, 2000). Another contributing factor to the expansion of state control over the economy in this period was the socialist leaning of the prime minister Mir Ḥosayn Musawi and key elements in his cabinet (e.g., Behzād Nabavi). Furthermore, they were helped by the non-religious left, especially in the first two or three years (Ashraf, pp. 130-43). This environment led to pervasive government control of production, distribution, and foreign trade and exchange rate systems.

Exchange rate, trade, and pricing policies. A very important tool of economic policy, which had significant implications for the development and the efficiency of the manufacturing sector, was the introduction of a multiple exchange rate system (MER) after the Revolution. (Farzin, 1995; Amuzegar, 1997; World Bank, 1991). This led to the co-existence of the official (nominal) rate alongside several preferential exchange rates and the parallel market rate.

The introduction of MER put the government in a position of managing its foreign exchange receipts from the oil sector. In practice, this meant that the government could allocate foreign exchange resources in accordance with its political priorities. Imports were subject to different exchange rates depending on the type of imports and their users. By the mid-1980s, seven rates were in operation. The official rate was 70 riāls to a dollar or 10-20 times below the market rate in the mid-1980s. This was applied to imports of essential goods. Imports of capital goods and intermediate goods required by the public enterprises, however, benefited from preferential exchange rates. Although above the official exchange rate, these rates were considerably below the market rate. In addition, there was an active black market with a parallel exchange rate with a significant mark-up above preferential rates and particularly the official rate.

The MER provided implicit foreign exchange subsidies to those groups who had privileged access to the official and preferential exchange rates. Importers of essential goods, public enterprises, and Bonyāds (state-related foundations) were the main beneficiaries of MER. These groups had access to highly overvalued exchange rates (official rate and various preferential rates). The managers of public enterprises and Bonyāds that were the beneficiaries of foreign exchange subsidies had a vested interest in preventing any significant official devaluation of the Iranian riāl. They also had no incentive to improve the efficiency and competitiveness of their enterprises. In contrast, the private sector had only access to the parallel market for foreign exchange and was not capable of competing with the public sector. Above all, for much of the period the private sector could not use black market foreign exchange to import goods. Imports were simply banned.

The foreign trade regime also became highly complex in this period, with import protection provided through tariffs, quantitative restrictions, and variable exchange rates. Most imports were subject to a wide range of tariffs and taxes. According to the World Bank (1991, p. 55), “the sum of tariffs and taxes on many imports could exceed 500 percent of import value.” Furthermore, protection was determined on a case by case basis, and imports were subject to a highly differentiated protective structure. Tariff rates could vary between zero and 100 percent for imports within the same classification, and the commercial benefit tax rate varied as widely as between zero and 400 percent (Alizadeh, 1992). Nevertheless the main instrument of protection was the dominance of the MER and particularly overtly overvalued official and preferential exchange rates. This meant that the managers of public enterprises and Bonyāds were the recipients of substantial implicit subsidies because of their access to the official and various preferential rates. Hence, the import requirements of these enterprises were obtained at artificially low prices.

The government almost determined prices of industrial outputs on a cost-plus basis, and wholesale and retail prices were also fixed by the authorities (Amuzegar, 1997, p. 204). Such price-fixing practices, which intended to reduce the galloping inflationary pressures, further eliminated necessary incentives for enterprise managers to cut production costs or increase their efficiency.

Subsidization of public enterprises provided little incentive for private investment in the manufacturing industries during the 1980s (Amuzegar, 1997, p. 204). Futhermore the disincentivization of the private sector was accentuated as foreign exchange shortages in the mid-1980s reduced the foreign exchange allocation for the private sector. This implied that the private sector could not satisfy its import requirements of intermediate and capital goods. This in turn had detrimental effects on capacity utilization in manufacturing enterprises, particularly in the private sector. Not surprisingly, manufacturing industries during the 1980s endured low levels of investment, shortages of skilled workers, and obsolete technology. Capacity utilization in the manufacturing sector during the 1980s was reduced to 58 percent from 80 percent or more in the mid-1970s (World Bank, 1991).

Iran’s industrial policy in the 1980s ran counter to that of many other developing countries in Latin America, Asia, and Africa that opted for market-oriented reforms (Alizadeh, 2003). These reforms, among others, included a dismantling of quantitative import restrictions, lowering of tariffs, relatively unified tariff rates for all commodities, and broadly speaking a more simplified trade and exchange rate system. These market-oriented reforms, which were aimed at improving the efficiency and productivity of the industrial sector, were concurrent with the reduction of the pervasive role of the state in the economy, a greater role for the private sector, and greater openness to the international economy. Iran’s experience in this period pointed in another direction.

RECOVERY AND GROWTH

The first five-year development plan (FFYDP), 1989-93. By the end of the Iran-Iraq War Iran had formulated its ambitious post-war reconstruction policies in the form of its First Five-Year Development Plan, FFYDP (1989-93). This plan reflected a significant departure from the earlier condition of industrial neglect (Pesaran, 2000). It set a growth target of 14.2 percent per annum for the manufacturing sector during the plan period (World Bank, 1991). This optimistic growth target was based on the expectation of higher capacity utilization and completion of unfinished projects.

The most significant aspect of FFYDP was in the field of trade and exchange rate policies (Pesaran, 2000, pp. 66-67). The first step in the design and implementation of the exchange reform was the simplification of the exchange rate, which involved a move from the seven-rates system of the late 1980s to a three-rate system in 1991. This consisted of: the official exchange rate at 70 riāls to the dollar, the competitive rate at 600 riāls to the dollar, and the free market rate, which was 2,000 percent of the official rate in the early 1990s (Hakimian and Karshenas, 2000, p. 61). In the next phase, the exchange rate was unified for a short period in 1993. Unification, however, proved short-lived. Accumulation of a very high level of short-term, external debt combined with the inability of the Iranian government to access long-term loans from multilateral organizations such the World Bank and the IMF led to a foreign debt crisis. The reason for the failure of exchange rate unification has received considerable attention in the literature (Farzin, 1995; Hakimian and Karshenas, 2000; Mazarei, 1996).

The FFYDP also attempted to promote the private sector, and plans were drawn up for the privatization of some 400 firms. Furthermore there were efforts to simplify the trade regime by removing some of the quantitative restrictions on imports. The plan also intended to deepen the process of industrialization by focusing on the production of intermediate goods (such as iron and steel, non-ferrous metals, paper products, synthetic fibers, chemicals and fertilizers) and capital goods (most notably, agricultural machinery, transport vehicles, electrical machinery, and power generation equipment).

About 70 percent of investment in the manufacturing sector was to be allocated to intermediate products, 20 percent to capital goods, and 10 percent to consumer goods (World Bank, 1991). This emphasis on domestic production of intermediate and capital goods was the continuation of the earlier policy, which intended to reduce the import dependency of the manufacturing industries.

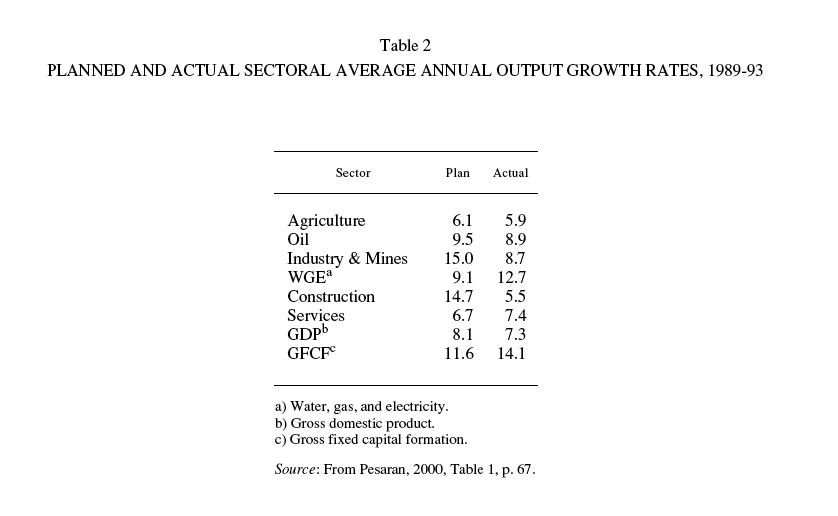

An assessment of the failure or success of these policies is hampered by the lack of disaggregated data on investment patterns in the manufacturing sector. The available data only allows for a comparison of the planned and actual growth rates for the industry and mining sectors over the plan period (see Table 2).

{kind=link}

The average planned growth rate for the industry and mining sector, which mainly consists of the output of the manufacturing sector over the plan period, was 15 percent. The actual growth rate for this sector, however, was only 8.7 percent over this period. Furthermore, the actual growth performance of the sector was closer to the planned growth rate in the first half of the plan than in the second half. According to Pesaran (2000, p. 68), the relatively high growth rate of the sector in the first half of the plan reflected the initial effects of the trade and foreign exchange liberalization. With the removal of trade and foreign exchange restrictions, private consumption grew very rapidly in 1990/91 and 1991/92. The high growth of manufacturing output during the first three years of the plan was accompanied by increasing utilization of existing capacities and increased imports. With the mounting debt crisis and the lack of access to international capital markets for long-term loans, the manufacturing sector was adversely affected by the foreign exchange constraint.

The second five-year development plan (SFYDP), 1995-99. The Second Five-Year Development Plan was launched in 1995. One of its key objectives was the adoption of a managed, unified floating exchange rate (Bank Markazi Iran, Economic Trends, 1379). Alongside this policy, the plan also aimed at streamlining the trade regime, to promote non-oil exports and revitalize the industrial sector. The target growth rates were much reduced compared with the First Plan. This reflected the foreign exchange constraint that the country was facing during a period of debt restructuring and lack of access to foreign credit.

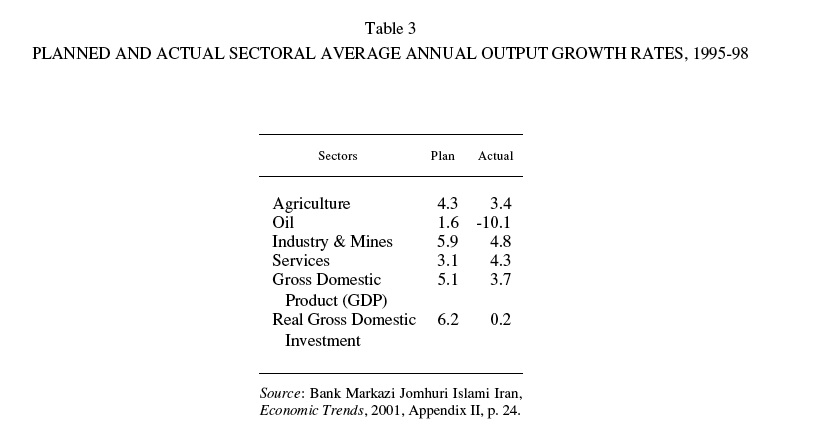

As can be seen from Table 3, the target growth rate was only moderately above the actual growth rate during the first four years of the plan period. In terms of investment, however, the Second Plan fell considerably short of its target, reflecting, among other things, the inability of the government to attract large private investment into the manufacturing industries (Zonuz, 2003).

{kind=link}

Despite the stated objective of exchange rate unification, the MER, which implied continued subsidization of public-sector as well as some private-sector manufacturing enterprises, remained in force during the Second Plan. It was not, in fact, until 2002 and in line with the Third Five-Year Development Plan that exchange rate unification was effectively implemented (IMF 2002a; Alizadeh, 2003)

The Third five-year development plan (TFYDP), 2000-2004. Since early 2000, the Iranian government has instituted a number of market-oriented reforms, including exchange rate unification, trade reforms, ratification of the law on foreign investment, tax reforms, and the licensing of three private banks (IMF, 2002a). It has also applied for membership in the World Trade Organization (WTO). These policies are intended to reduce the system of subsidies and protection, streamline the administrative red tape, and to promote the role of the private sector. The focal point of the reform program has been exchange rate unification, which was designed to rectify the system of implicit subsidies and distortions mentioned previously. Exchange rate unification to this date has remained intact. The stages involved in the removal of implicit subsidies to state-owned enterprises, as a result of exchange rate unification, received due attention (IMF, 2002a; Alizadeh, 2003).

The Third Plan has been more focused on industrial development than previous plans. Certain distinctive features of industrial policy in the TFYDP are: emphasis on increased domestic and international competition, provision of cheap, institutionalized credit to promote investment in the private sector, acceleration of privatization policies, and much greater concentration on non-oil exports (Sāzmān-e modiriat o barnāmarizi-e kešvar, 2003, I, pp. 46-52; II, part 2, pp. 1369-1423).

The formulation of policies for the removal of state monopolies in the production of sugar and tobacco, removal of non-tariff barriers, reduction of tariff for several steel products, and import liberalization for a number of products are in the direction of increasing domestic and international competition. There has also been realization that the growth of private investment in the manufacturing sector has been slow. Consequently, there is an attempt to promote private investment through the provision of preferential interest rates by the banking sector. The government also intends to make the public a stakeholder in manufacturing industries through the sale of shares of state-owned industries, including petrochemicals and handicraft industries, to the public. This policy is also designed to increase the contribution of the stock market in provision of funds for industries. In the Third Plan there is also combined emphasis on resource-intensive industries such as petrochemicals and steel (which were also of importance in previous plans) as well as on electronics and other high tech industries.

It is difficult to assess the effectiveness of these policies at this stage. Nevertheless, the performance report on the Third Development Plan indicates that in the first three years of the plan, 2000-2002, the actual growth rates of the manufacturing and mining sector exceeded the target rates (Table 4)

{kind=link}

In actual fact the manufacturing and the mining sector outperformed the plan’s prediction, although the target growth rates for the sector were moderate, closer to the Second than the First Plan. Ironically this relatively high growth rate was achieved despite relatively limited growth of investment in the sector in the second and third year. One possible explanation for this situation is increased capacity utilization arising from exchange rate unification and the removal of acute foreign exchange constraint over this period. Another distinctive feature of the Third Plan is its emphasis on non-oil exports.

Although official emphasis on non-oil exports is not new, nevertheless the export promotional policies in the Third Plan appear to be more vigorous than in the two previous plans. This is reflected in the performance of non-oil exports, which outperformed their target rate for the first nine months of 2003 (Table 5).

{kind=link}

As is clear from the table, industrial goods and petrochemicals are the major components of non-oil exports, while the share of carpets and handicrafts—traditional non-oil exports—amount to less than 10 percent of the total export of goods. The performance of non-oil exports varies. Industrial and agricultural goods outperformed their target rates, while other non-oil goods exports, including petrochemicals, underperformed. Another component of non-oil exports is export of services, which include engineering and technical services (to neighboring countries) as well as tourism and transport.

Employment. There has been a sharp rise in the unemployment rate since the revolution, although the sectoral distribution of unemployment is not known (Alizadeh, 2003). The overall unemployment rate, which was 3.6 percent of the labor force in 1976, increased to a two-digit figure by the early 2000s.

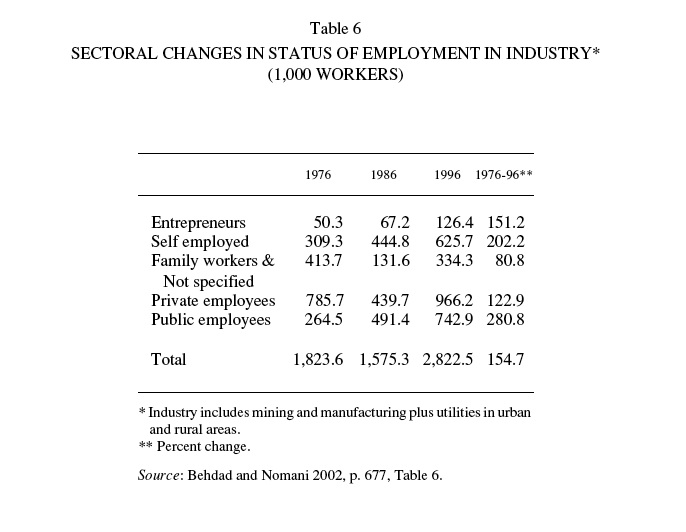

Table 6 shows sectoral changes in the status of employment in industry (both urban and rural) in 1976, 1986, and 1996. A few trends are reflected in this table. Firstly, the neglect of the manufacturing industry in the 1980s is reflected in an absolute decline in employment in this sector from 1,823,600 in 1976 to 1,575,300 in 1986. Employment in the industrial sector, however, has increased since the mid-1980s. The next visible trend is the rapid expansion of public employment, which reflects large-scale nationalization of the manufacturing enterprises after the revolution. This trend, however, is more pronounced over the period of 1976-86 (when public sector employment nearly doubled) than in the later period of 1986-96.

{kind=link}

Another noticeable change is the declining share of employment in the private sector, although employment in the private sector has been increasing more rapidly than that of the public sector since 1986. The data in the table also point to a rapid growth in self-employment over the entire period. Self-employment accounted for 309,300 out of 1,823,600 for the total employment in industry in 1976. This is equivalent to 17 percent of the total em-ployment in that year. By 1996 self-employment was responsible for 23.1 percent of the total industry employment (i.e., 652,700 in self-employment out of the total employment of 2,822,500 in industry). The rapid growth of self-employment is not surprising. According to IMF (2002a, 2002b) reports on Iran, the public sector, which accounts for the major share of industrial output, has been incapable in generating employment opportunities for a growing population.

OVERALL ASSESSMENT

Efficiency, fragmentation, and concentration. Since 1980, the Iranian industrial scene has been dominated by highly subsidized, inefficient, and overstaffed state-owned enterprises (SOEs). These SOEs account for 70 percent of industrial value-added or about 15 percent of GDP (IMF, 2002a, pp. 73-76). There is a dearth of information about the financial situation of SOEs. However, available data suggests that a large number of them have been operating at a loss and are highly dependent on substantial government subsidies. It is estimated that the financial losses of selected state enterprises amounted to 51 percent of their total revenue in the period 1994-99, which is equivalent to 2.7 percent of GDP over this period (IMF, 2002b). These losses were financed in part through budgetary transfers and in part through bank loans.

The dire financial condition of public manufacturing enterprises has been a matter of longstanding concern and the main factor behind the privatization drive since the FFYDP (World Bank, 1991; Zonuz, 2003). Actual progress in the area of privatization has been slow, even though the legislative and regulatory environments governing privatization have been in place for some time (IMF, 2002b; Zonuz, 2003).

The Third Development Plan appears to be more concerned than previous plans with industrial growth, increased competition, expansion of the private sector, and improved efficiency. The revival of the stock market since 1989 and its rapid growth in recent years reflects the changing landscape of industrial development in Iran.

Despite these noticeable developments, manufacturing industries are still subject to an unfavorable environment that hampers the realization of their full potential. Indeed, industrial policies have failed to attract ‘big’ private capital, domestic or foreign, to the manufacturing industries. This is not to deny that private investment has been expanding rapidly in recent years in several manufacturing industries, including consumer durables (cars and automotives), building materials (tiles, sanitary ware), food processing, and electronics (e.g., computer monitors). Nevertheless most newly established private firms are involved in assembly of household appliances at a relatively small scale (Alizadeh, 2003). The reluctance of domestic/foreign firms to invest in large-scale manufacturing activities in Iran (comparable with the pre-revolutionary period) is not only a response to massive nationalization after the revolution but also the lack of a favorable environment for industrial development.

Rigidity of labor relations reflected in the enactment of the labor law in 1990 has increased the cost of hiring and firing (Alizadeh, 2003). Also the economic and political power of Bonyāds to manipulate policies has undermined the credibility of government industrial policies. The issue of ‘policy credibility’, which is of crucial importance in investment decision by the private sector, is further aggravated by the continuing power struggle within the establishment (i.e., between the ‘conservatives’ and ‘reformists’ factions as well as infighting within each of those factions between ‘ideologists’ and ‘pragmatists’). This politically unpredictable environment is not particularly conducive to the activity of large-scale development by private capitalists.

The lack of relevant data does not allow for a comparative analysis of the scale of investment in various manufacturing industries in the pre- and post-revolutionary revolutionary periods. Nevertheless there is some indication of the fragmentation of the manufacturing industries.

A well-known case is the automobile industry, which is far more fragmented now than in the pre-revolutionary period (Valibeigi, 2003). The industry, which is highly susceptible to economies of scale, is characterized by the prolongation of sub-optimal plant size, and the proliferation of a large number of assembly plants and a considerable number of brands. All firms in industry are engaged in producing a fragment of the market. There has been no attempt at rationalizing the structure of the industry. This pattern is in contrast to the structure of the industry in the pre-revolutionary period, when one firm in the auto industry (i.e., Iran National) and another one in the commercial vehicle sector, in particular the production of trucks (Ḵāvar company), were the dominant producers. These two firms accounted for 60-80 percent of the total production of autos and commercial vehicles before the revolution (Alizadeh, 1985). Although there were a number of others in the industry, the production of autos and commercial vehicles was concentrated in the two above-mentioned firms. Under the guidance of Industrial, Mining and Development Bank of Iran, IMDBI, they also increased their use of locally manufactured components. IMDBI, a highly influential development bank, which was providing cheap institutionalized credit to the large private firms, also monitored their performance. Provision of loans was made conditional on progressive increase in local components as well as on upgrade of the borrowers’ technical expertise. By late 1970s virtually 50 percent of the parts and components of the vehicles produced by these two leading firms were made locally. Although the industry was private it was far more rationalized (in terms of minimum efficient plant size) then than since the Islamic revolution. Ironically the nationalized automotive industry since the revolution has been far more fragmented, as large numbers of firms have been mushrooming in the industry. Furthermore the degree of vertical integration of the industry has been considerably reversed. Current evidence suggests that the industry is far more dependent on imported parts and components now than in the earlier phase (Valibeigi, 2003). This is not surprising. The production of parts and components is highly susceptible to economies of scale, and coexistence of a large number of brands and small producers does not allow for the utilization of scale economies. Under such conditions, the domestic production of parts and components, which could increase the per-vehicle production cost several folds, is not encouraged.

Is this trend towards fragmentation specific to the automotive industry, or is it a more widespread pattern in the post-revolutionary period? In the absence of relevant information it is difficult to provide comparative analysis of the extent of industrial concentration in the two periods. Nevertheless, there is certain indication that fragmentation is not confined to automotive industry but is widespread in the industrial sector and within the whole economy. A study by Behdad and Nomani (2002) indicates that there has been a decline in the concentration of capital in the economy as a whole. They define Concentration Index (CI) as the ratio of private employees per entrepreneur in various sectors. In 1976, the CI for the industry was 11.7. By 1986 this index had declined to 5.2. Although by 1996 CI was 6.1, and hence slightly higher, the index has remained considerably below its pre-revolutionary phase. They argue that the decline in CI is indicative of the retrenchment of capital in the post-revolutionary period. The main implication of the decline in concentration ratio is dominance of smaller firms since the revolution. This is a worrying trend, given that a trend towards concentration of capital and large-scale production is a required condition for a successful industrial takeoff.

Bibliography:

Parvin Alizadeh, “The Process of Import-Substitution Industrialization in Iran with Particular Reference to the Case of Automotive Industry (1960-1978),” unpubl. D. Phil. diss., Institute of Development Studies, Sussex University, UK, 1985.

Idem, “Industrial Development in Iran,” Middle East Study Series 31, Institute of Development Economics, Tokyo, 1992, Table 4, p. 179.

Idem, ed., The Economy of Iran: Dilemmas of an Islamic State, London, 2000.

Idem, “Recent Economic Reforms and Structural Trap: Iranian Quandary,” The Brown Journal of World Affairs 9/2, Winter/Spring 2003, pp. 267-81.

Houshang Amirahmadi, Revolution and Economic Transition: The Iranian Experience, Albany, 1990.

Jahangir Amuzegar, Iran’s Economy under the Islamic Republic, London, 1997.

Ahmad Ashraf, “Charisma Theocracy, and Men of Power in Post-Revolutionary Iran,” in M. Weiner and A. Banuazizi, eds., The Politics of Social Transformation in Afghanistan, Iran, and Pakistan, Syracuse, 1994, pp. 101-55.

Bank Markazi Iran, Economic Trends, Tehran, various issues, 1980-2003.

Sohrab Behdad, “From Populism to Economic Liberalism: The Iranian Predicament,” in Alizadeh, ed., 2000, pp. 100-145.

Idem and Farhad Nomani, “Workers, Peasants, and Peddlers: A Study of Labor Stratification in the Post-Revolutionary Iran,” International Journal of Middle East Studies, 34, 2002, pp. 667-90.

Y. H. Farzin, “The Political Economy of Foreign Exchange Reform,” in Said Rahnema and S. Behdad, eds., Iran after the Revolution: Crisis of an Islamic State, London, 1996, pp. 174-203.

Hassan Hakimian and Massoud Karshenas, “Dilemmas and Prospects for Economic Reform and Reconstruction in Iran,” in Alizadeh, ed., 2000, pp. 29-62.

The International Monetary Fund (IMF), Islamic Republic of Iran, Staff Report for 2002 Article 1V Consultation, Washington, IMF, 2002a.

Idem, Islamic Republic of Iran, Selected Issues and Statistical Appendix, IMF Country Report No. 02/212, Washington, D.C., 2002b.

Adnan Mazarei, “The Iranian Economy under the Islamic Republic: Institutional Change and Macroeconomic Performance, 1979-1990,” Cambridge Journal of Economics 20, 1996, pp. 289-314.

Hashem Pesaran, “Economic Trends and Macroeconomic Policies in Post-revolutionary Iran,” in Alizadeh, ed., 2000, pp. 63-99.

Sāzmāne modiriyat wa barnāmarizi-e kešvar, Gozāreš-e eqteṣādi-e sāl-e 1381 wa neẓārat bar ʿamalkard-e se sāl-e awwal-e barnāma-ye sevvom-e tawseʿa (Economic report 2002 and the first 3-year performance report of the 3rd development plan) II/2, 2003, Table 1.

Ḥasan Wālibeygi, “Barrasi-e ʿamalkard-e ṣanʿati-e qaṭʿa sāzi-e ḵodro” (Survey of the performance of Iranian auto parts manufacturing), Barrasihā-ye bā-zargāni 1/2, 2003, pp. 3-19.

“Ważʿiyat-e ṣāderāt-e Irān dar noh māh-e Farvardin leḡāyat-e pāyān-e Dey māh-e sāl-e 82” (Iran’s export in the first nine month from April-January 2003), in Payām-e ṣāderāt 7, 2003, p. 27.

World Bank, “Iran: Reconstruction and Economic Growth,” Country Operation Division, Report No. 9072-IRN, I, July 1991.

Behruz Hādi Zonuz, Tajroba-ye siāsathā-ye ṣanʿati dar Irān, 1374-1380 (Iran’s industrial policies in practice, 1995-2001),

Markaz-e taḥqiqāt-e Majles (Majlis research center), Tehran, Iran 2003.

(Parvin Alizadeh)

Originally Published: December 15, 2004

Last Updated: December 15, 2004

This article is available in print.

Vol. XIII, Fasc. 2, pp. 119-125

Parvin Alizadeh, “INDUSTRIALIZATION iii. The Post-Revolutionary Period, 1979-2000,” Encyclopaedia Iranica, XIII/2, pp. 119-125, available online at http://www.iranicaonline.org/articles/industrialization-3 (accessed on 30 December 2012).